- Real Estate 3.0

- Posts

- The Great Unbundling of Banks... and the Rise of On-Chain Companies

The Great Unbundling of Banks... and the Rise of On-Chain Companies

For most of modern history, finance was built around institutions that controlled everything. Banks held deposits, issued loans, processed payments, safeguarded assets, and distributed financial products. The entire system was vertically integrated. If you wanted to interact with the financial system, you did so through a bank. Then the internet arrived, and the dynamic changed.

Yacine Terai

March 18, 2026

This model dominated for decades because finance required infrastructure that was difficult to build and expensive to operate. Regulation, capital requirements, and technological barriers meant only large institutions could manage the full stack of financial services.

During the past fifteen years, a new generation of fintech companies began dismantling this model piece by piece. Instead of building full banks, startups targeted specific functions that banks had historically bundled together. Stripe focused on payments. Wise tackled cross-border transfers. Robinhood reimagined retail investing. Affirm reinvented consumer lending.

Each company extracted one service from the traditional banking bundle and rebuilt it with better software and simpler interfaces.

This process became known as the “unbundling of banks.” But the story did not stop there.

The deeper transformation came from the emergence of financial infrastructure built around APIs and programmable systems. Banking-as-a-Service platforms allowed companies to integrate financial services without becoming banks themselves. Payment processing became a software layer. Financial services became composable.

Finance was no longer defined by institutions. It became defined by infrastructure.

Today, a similar transformation is beginning to unfold in another domain that has historically been even more rigid than banking: company ownership and asset management.

The traditional architecture of a company is surprisingly complex. When someone creates or operates a business or owns a valuable asset, the structure typically involves multiple intermediaries and fragmented systems. Lawyers incorporate the entity. Banks manage accounts. Share registries track ownership. Brokers facilitate transfers. Accountants maintain records. Custodians safeguard assets.

Each component of the system lives in a different database, maintained by different institutions.

This architecture was designed in a world where trust had to be mediated by centralized parties and where digital infrastructure did not exist. Ownership records were paper-based, then digitized in siloed systems, but the fundamental structure never changed.

Blockchain technology introduces a different possibility.

Instead of relying on fragmented registries and intermediaries, ownership can now be represented directly on programmable infrastructure. Digital tokens can represent shares, assets, or economic rights. Smart contracts can enforce rules that previously required legal coordination across multiple institutions. Transfers can happen instantly, globally, and transparently.

What APIs did for fintech, blockchain is beginning to do for ownership.

Assets, companies, and financial rights are becoming programmable objects.

This shift is part of a broader transformation often described as the tokenization of real-world assets. Real estate, equity, infrastructure, and private market investments are gradually moving toward digital representations that can be issued, transferred, and managed on-chain.

But the most important change is not simply digitization. The real transformation lies in the restructuring of the ownership stack itself.

When companies and assets become programmable, the layers of ownership management can be rebuilt from the ground up. Legal structures, registries, settlement systems, and distribution channels can be integrated into a single digital framework.

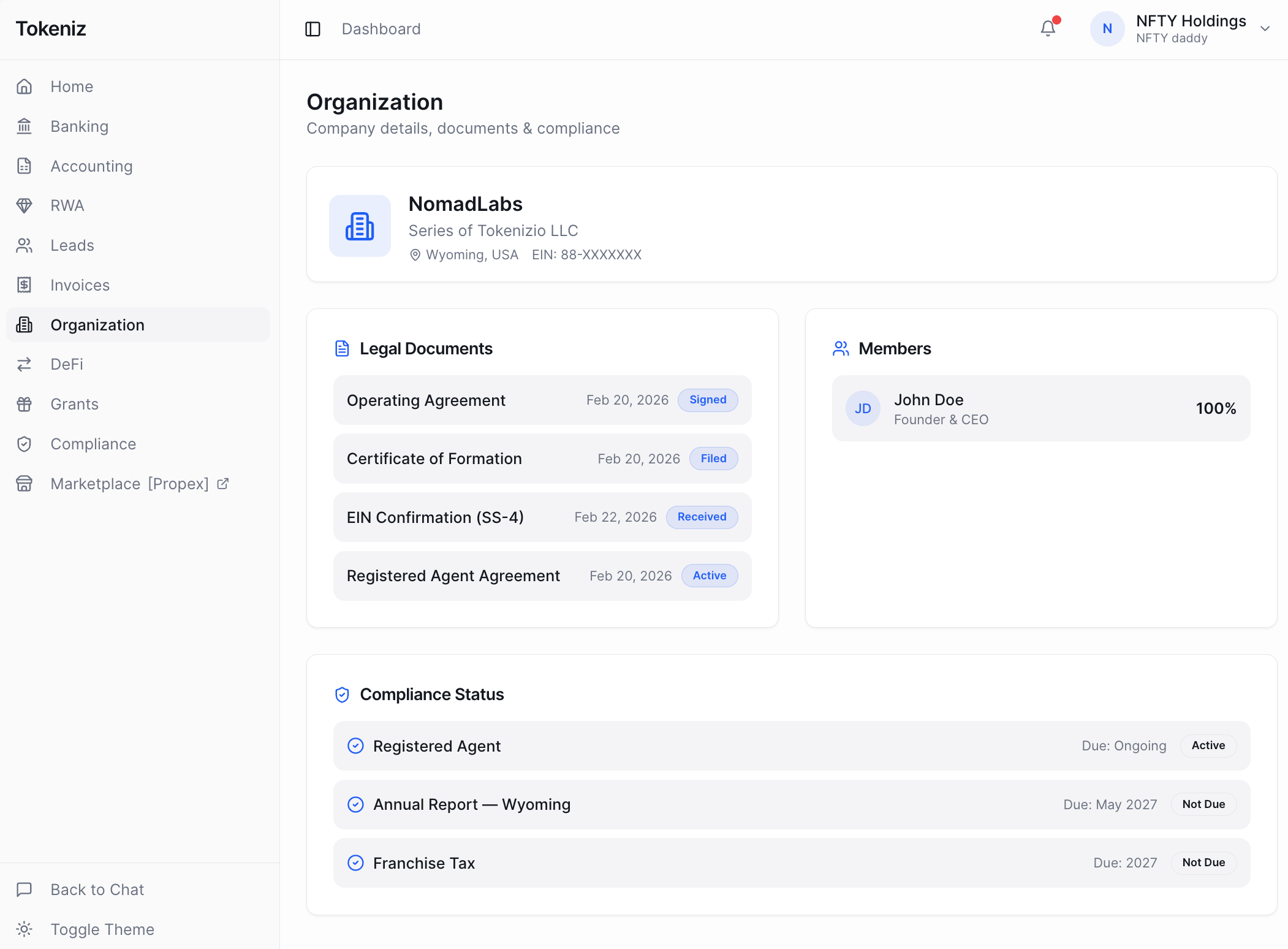

In this emerging architecture, platforms such as Tokeniz are positioning themselves as infrastructure for the next generation of digital companies.

Tokeniz is designed around a simple idea: if businesses and assets increasingly live on the internet, their legal and ownership structures should also exist in a digital-native form.

Through structures such as tokenized Series LLCs, ownership can be represented directly through blockchain-based tokens while remaining anchored in compliant legal frameworks. Each asset or venture can be structured as its own legal entity, while the ownership of that entity can be transferred, fractionalized, or distributed digitally.

This approach transforms the company itself into a programmable container for ownership.

Just as Stripe allowed developers to integrate payments into software with a few lines of code, the next wave of infrastructure platforms aims to make ownership composable and interoperable across digital systems.

For entrepreneurs, this means companies can be launched, financed, and managed in a far more fluid way. Ownership can be distributed globally. Liquidity can be introduced in traditionally illiquid markets. Assets that once required large capital commitments can be fractionalized and accessed by broader groups of investors.

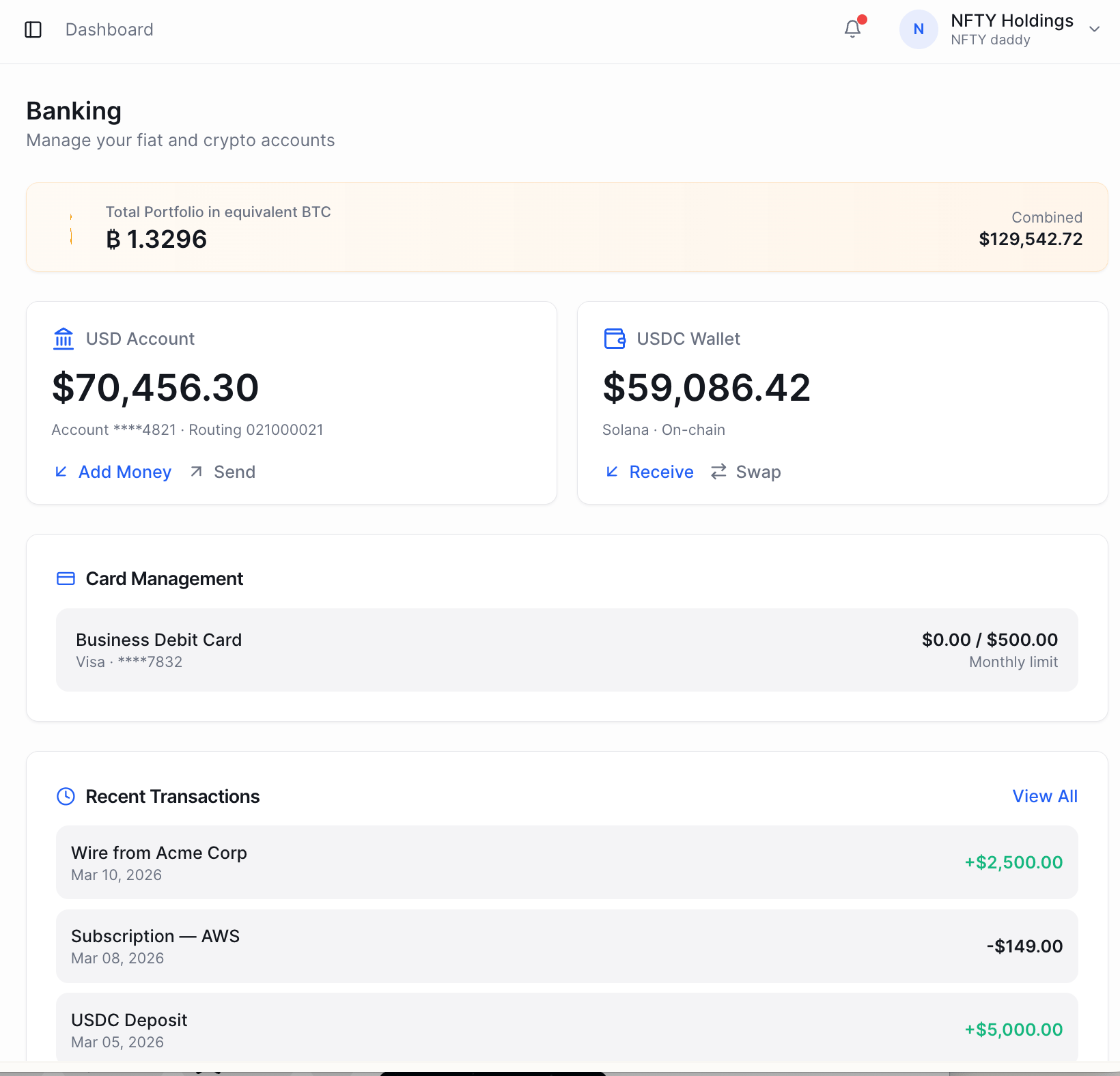

Tokeniz dashboard

For investors, it opens access to markets that were historically restricted to private networks and institutional capital. Real estate, private equity, infrastructure projects, and other real-world assets can become part of a more transparent and accessible financial ecosystem.

In this sense, the tokenization of companies and assets represents the continuation of a broader historical trend. Every major technological shift reorganizes economic infrastructure. The internet reorganized information. Software reorganized services. Fintech reorganized financial distribution.

Blockchain has the potential to reorganize ownership itself.

The unbundling of banks showed how powerful infrastructure shifts can be. When the foundations of finance change, entirely new categories of companies emerge.

Today we may be witnessing the beginning of a similar transformation, not just in financial services but in the structure of economic ownership.

If the first generation of fintech companies rebuilt the interface to finance, the next generation of platforms may rebuild the infrastructure of ownership.

In that world, companies are no longer static legal structures created once and managed through paperwork and intermediaries. They become programmable digital entities capable of interacting directly with the internet of value.

The unbundling of banks was only the beginning.

The next transformation may be the rebundling of companies themselves—on-chain.